It was a few years ago while studying for my CFP® credential that I first encountered the concept of Human Capital. Essentially, Human capital is the present value of all future potential income you will earn throughout your career. When you are young, your Human Capital is usually the most valuable asset that you have. Anything you do to increase your ability to earn higher future wages could be considered investing in your human capital. The investments that you make early in life, like obtaining a higher education, on-the-job training etc can increase your personal human capital.

In the area of Protection, Life cover and Risk Management, Human Capital has caused many financial advisers to alter their current thinking on the most appropriate levels of life assurance and protection. The financial position of most clients can be split into two distinct parts, Financial Capital and Human Capital. As advisers are usually very familiar with the Financial Capital of our clients. Financial Capital is an umbrella term which represents a clients’ financial assets, investments, pensions etc. We are all trained to critically assess financial capital and so we become adept at projecting Pension fund values and comparing investment funds. However, this only gives us a partial view of our clients’ financial position. We rarely assess in any great detail the most valuable asset that our clients possess, their future income or Human Capital.

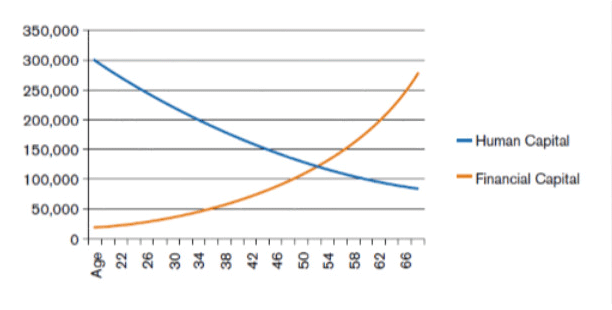

The image below shows the inverse relationship between Human Capital and Financial Capital during a typical working life cycle. If we examine this chart closely, it opens up many interesting areas of discussion. Human Capital can help us addresses some very important and common questions in a new way.

How much life cover is enough to protect my family? And what type of Life cover should I have?

When you are a young adult, it is very important to protect your human capital with both life and serious illness policies. Doing so will protect you and your family against a possible human capital shortfall, due to an untimely death or a career-ending illness. This is especially true if your expected future financial obligations are high. As you get older, your need to hedge your human capital with insurance, should decrease. As you can see from the attached image, after the point of intersection between Human capital and financial capital, the need for additional life insurance decreases dramatically.

Where should I invest my savings?

Linking an appropriate investment strategy to the concept of Human Capital is new to most of us, but very relevant. If we agree that a client’s Human Capital is their most valuable asset, then surely it should always be taken into consideration when making Investment decisions. Many people may have built up wealth through their employment, one example being bank employees accumulating bank shares in their employer. We have also heard many stories of retired bank staff that still had a huge portion of their pensions and savings in bank shares. During the downturn many have taken a double hit of job losses and investment losses coinciding. This is an example of a lack of diversification between Human and Financial Capital. Employees should compensate for this risk by investing their financial capital in industries and companies with little or no correlation to their human capital. One rule of thumb is that investors should have no more than 5% of their portfolios in one stock. But if that one stock is in the company that also puts food on your table, then even 5% might be too much. This ‘familiarity bias’ can be very dangerous. Theoretically, a

career civil servant should have their Financial Capital invested in reasonably high risk asset classes, as their Human Capital is secure. On the other hand, a self-employed individual with a new business should have their financial assets invested safely, to compensate for the volatile nature of their future income. In reality, the opposite is often the case.

Your human capital should always open to further investment, through more education and on-the-job training, after all, “The best investment you can make is always in yourself.”

Barry Kerr

Barry Kerr

Wealthwise Financial, Carrick-on-Shannon

www.wealthwise.ie